is it a bad time to buy a home?

We’re thrilled to be back with another real estate post today, and thought we’d tackle this little topic: Is it a bad time to buy a home? To answer this little FAQ that we seem to be getting a lot with our clients, we’re diving into numbers today. So if you’re ready to check it out, buckle up, buttercup.

I {Jamin} feel like a broken record when talking to clients who are interested in buying a home right now. Everyone wants to know if it’s a bad idea. Simply put, no it actually isn’t. Maybe it isn’t the right idea for you, but it’s also not a bad idea. And the easiest way to help understand this is by cutting out the noise and looking at the data.

1. I know the first objection: interest rates are high right now, so how can you justify buying and paying more? We’ve been saying the same thing for months now, {you can read about it here} but interest rates actually aren’t historically high, they are close to average. We were just spoiled over the last 5 years.

2. The second objection: which I’ll deal with below is… but what about the crashing housing market?

Total side note, but just remember this isn’t financial advice… just sharing what I see and why I don’t think the sky is falling.

source

This isn’t 2007/08 when it comes to supply. This chart shows the current available supply of housing in the US.

• New home building has never recovered from pre-2007, and, without a doubt there is a shortage of homes on the market that will continue for the foreseeable future. Yes, it will ease, but easing and overtaking demand are two very different things.

• This is combined with the fact that 82.4 percent of all current homeowners are locked in below the 5 percent interest rate mark. In fact, most of them are well below it which leads most homeowners to only move if necessary. We’ll see this in instances like a job or larger house, and not just because they can. That means that there will be less older homes coming to market.

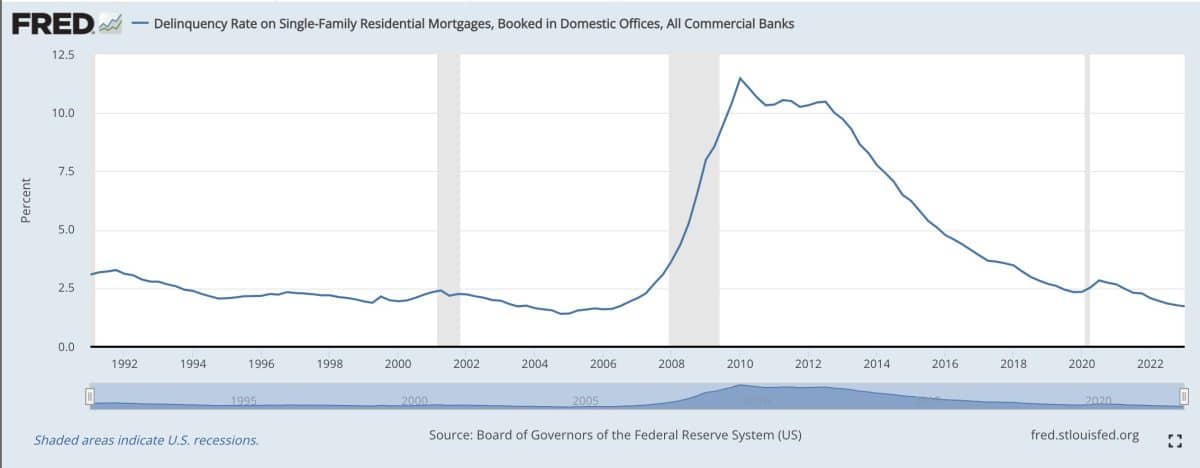

This isn’t 2007/08 when it comes to the default rate.

• Unlike the great housing crisis, Americans have more equity (more on this below) in their homes, and negative equity is at extreme lows, too. That means foreclosures are close to the lowest point in the history of our country.

• The current default rate on mortgages is at 1.78% compared to 11.48% at the height of the housing crash.

source

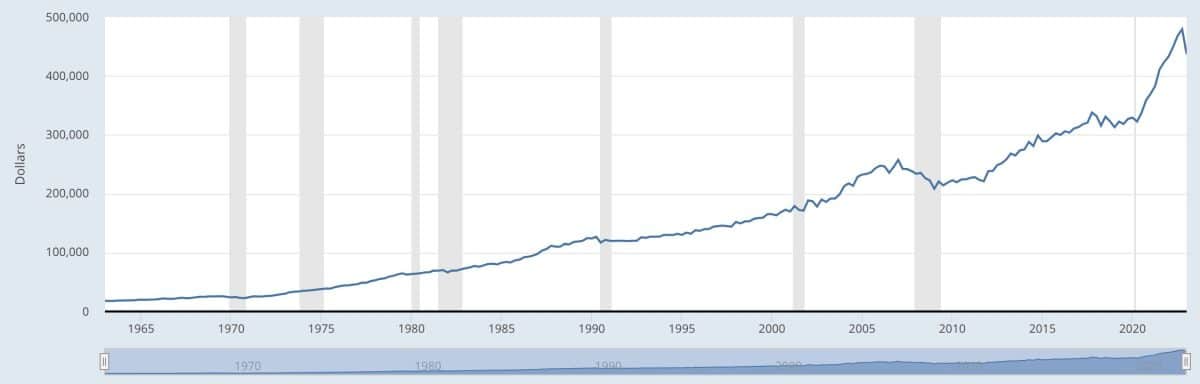

This isn’t 2007/08 when it comes to more savings and equity.

• Some estimates state that Americans added 2.3 trillion to savings during the pandemic. The home equity stake of the average American homeowner with a mortgage is worth just over $274,000, as of the first quarter of 2023. Both of these add up to Americans having more money saved and more draw-down power against their current home, which bolsters the above point about home mortgage defaults.

This isn’t 2007/08 when it comes to being blindsided.

• If you didn’t live through the housing crash of 07/08 then you don’t remember. In short, everyone {for the most part} was blindsided by the economic downturn. There was no media coverage before it happened, no one was prepared, and no one knew the talking points. Compare that to now. We have read and heard ad nauseam about the economic downturn, everyone knows Jerome Powell, and we all know the talking points. Which means we have all had ample time to prepare. Most people did, and are.

This isn’t 2007/08: So here’s the takeaway.

• The above 4 points lead me to believe we aren’t in danger of a housing crash. Could there be a downturn? Sure. But I think a crash is a fanciful dream by the bears of the market hoping to party like it is 2008. The current data just doesn’t support a crash or major loss of value. That matters, because if the market is about to crash you don’t want to buy.

So back to our original question: Is it a bad time to buy a home?

If we don’t anticipate a crash and interest rates really aren’t that much off their historical average, the answer at the very least has to be neutral. So how do you navigate a neutral market? By changing your mindset.

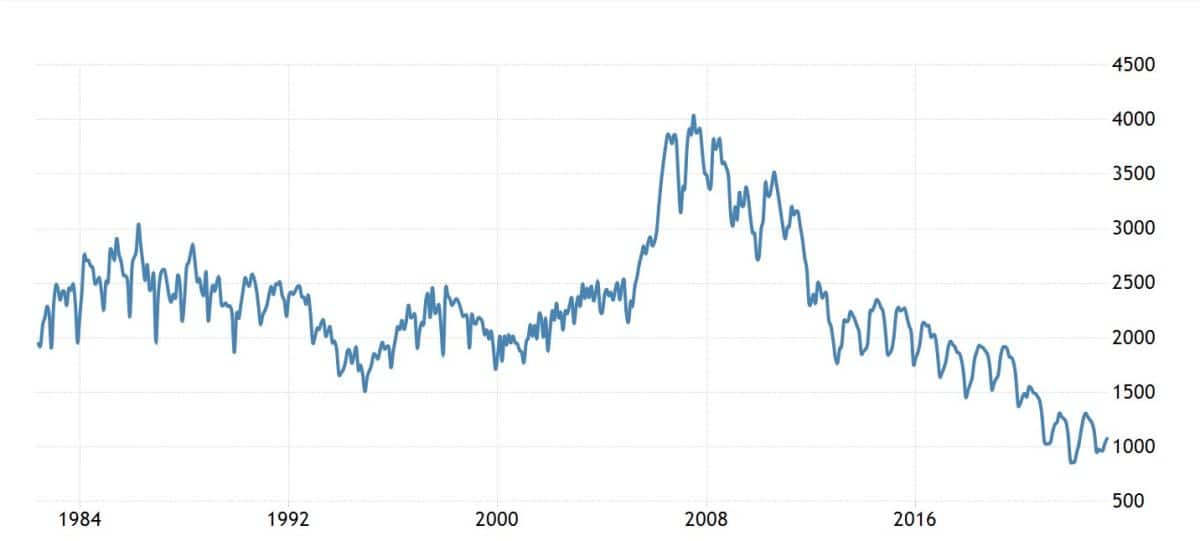

This is a historical home price chart.

The housing crash led to roughly an 18% dip in home prices which then rallied to a 32% increase in home prices over the next five years. The current market has led to a 10% dip in home prices. Could it go another 8-10%? Possibly. But that’s not the point.

Remember, during the crash of 08′ there was an abundance of supply in the homes available to purchase. That’s not the case now. So does it really make sense for a crash?

Historically, the chart moves up and to the left. So it’s safe to assume over any given 5-year period your investment will gain. Even during the highest interest we have known, 1980-85 home prices rose 29%.

This brings me to marrying the house and dating the rate. One of two things can happen: either you’ll sell the house in 5 years and realize a gain, or you can stay in the house and historically rates will be lower for you to refinance and you’ll realize even more gain in equity.

But look at it like this as well: Imagine you have the current 7% rate which is 4% more than a 3% rate of 2021. Historically over a 5-year period, your investment would still net you a 10% +- gain on the portion of the home you mortgaged (accounting for your higher interest rate.) and a 30%+- gain on the equity portion.

So let’s say you only put 20% down on a $400,000 home. That would mean over a 5-year period, you would historically gain 13%+- in equity. Even if home prices dipped to 2008/09 levels, you would still be to the good 5%+-. But as illustrated above, the data doesn’t support that dip. And if it does dip, guess what will happen? Interest rates will go down and you can refinance.

Lots to make your head spin, but hopefully something to think about as well.

Also, I would not advocate for everyone to buy right now. Some situations just don’t justify, but that is true in any market condition, which is why you need a professional Realtor to help you gauge the market in your area. Just remember there is never a one-size-fits-all.

All of these photos are from our Chapman Lane project! Be sure to check out this fun kitchen reno, + the rest of our portfolio, here.

________________

Real Estate is an interesting beast and having an agent that can pull the curtains back and help navigate what will most likely be the biggest purchase of your life, is essential. As they say, you don’t know what you don’t know, and that’s where a good realtor comes in. {If you need help in hiring a Realtor, check out our post here.}

If you’re in the Nashville area I’d love to help you and even if you aren’t, let us know we might be able to point you to someone great!

Be sure to check out the rest of our real estate series, here.

Contact us here to work with us + here to talk all things renovations!

Have an inspired day!