the future of the housing market

We’re thrilled to be back with another real estate post today and thought we’d tackle this little topic: Another look at the real estate market and how to navigate one of the biggest purchases of your life. If you’re in the market now or will be in the future, we want to provide you with valuable information for navigating the real estate market. We can help you make that next purchase. So let’s dive in, shall we?

I {Jamin here} want to dive into the future of the housing market and what I believe we can expect as we move into 2024. Let’s get this out of the way first, but please understand we’re not offering personal financial advice here. We highly encourage you to talk to your local Realtor and licensed financial adviser. (Side note: If you need help finding a good local Realtor, let me know, we have helped several people with this not-so-little task.)

So with that out of the way, let’s jump into our dubious speculation on the future of the housing market.

The future of the housing market: Working Theory

Our working theory/premise is that we will begin to see an uptick in the housing market in January/February as sales and home values ramp up through the rest of 2024 and into 2025.

We will cover below why we think 2024 is the time to buy, and what signals we think the broader market is giving to support this view.

The future of the housing market: Almighty FED

If you live in a bubble and have missed the frenzied pace at which the FED has hiked the FED funds rate, then lucky you for just coming out of hibernation as it seems to be near if not at the terminal rate. Market watchers believe the current estimate that the FED will hike rates again at their December meeting to be a 1 in 20 chance. That’s good news for mortgages.

Why is that good?

Here’s a quick economic lesson, because you know we learn Trig instead of basic life skills in school, but digression. The FED funds rate is the base rate at which money is borrowed against. So for our discussion, it drastically affects mortgage rates. If the FED is at or near the terminal rate that would lend to the belief that mortgage rates will be stabilizing, if not going even slightly lower, shortly.

We are in the part of the FED cycle that is known as quantitative tightening or QT for short. This is simply when the FED removes securities and other items from their balance sheet, and raises the FEDS funds rate in an attempt to slow the economy down to reign it in, and in our case, get inflation down.

At some point and we may be at that point, the FED pauses, holds, and then turns to QE or quantitative easing where the FED purchases securities, and lowers the FED funds rate all in an attempt to stimulate the economy. Well, at least that’s an oversimplified explanation.

The pie-in-the-sky hope is that the FED lowers inflation without doing much damage to the economy and sending it into a recession or a mild recession at best. This is known as a soft landing.

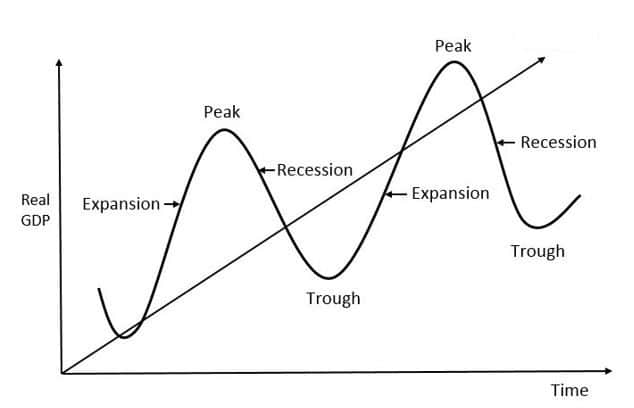

Econ 102: Business cycles are a real thing y’all and there are four parts. Guess which part we’re in? Here’s a little key to the graph below.

Expansion: Output is growing

Peak: Turning point between expansion and contraction of output

Recession: The phase in which output is falling.

Trough: Turning point between contraction and expansion

In 2020 and 2021 and the first part of 2022, we were in an expansion phase. And in mid-22 until now, we have been peaking if not beginning our recessionary journey into early 2024. I don’t believe we will spend much time if any meaningful time there. I believe as several leading economists have indicated that we might have achieved a soft landing. The FED has preached higher for longer, meaning getting the rates higher and then holding them for longer, which I believe lends itself to a lengthened trough.

A lengthened trough will slow the economy enough to bring back QE or what the news likes to call money printing. This all matters because QE lowers interest rates, which of course affects home buying.

The future of the housing market: Supply.

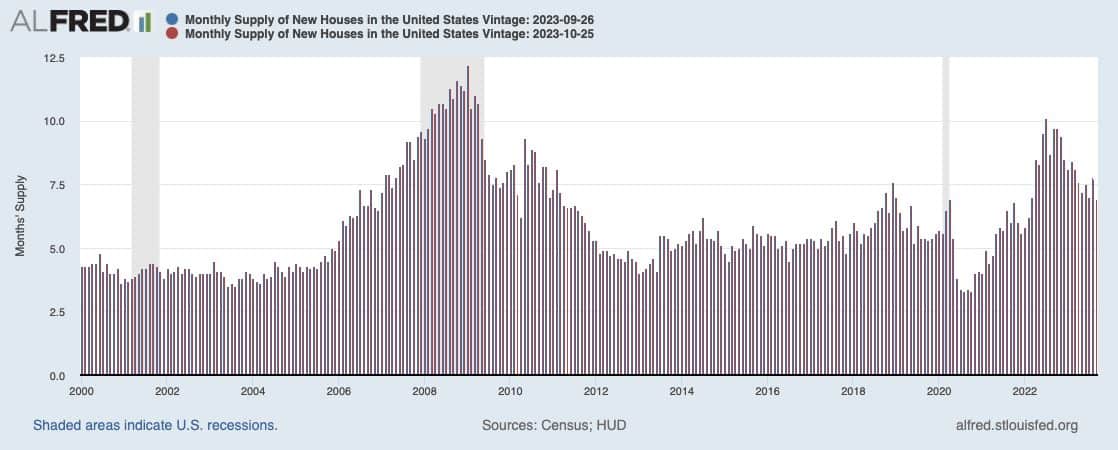

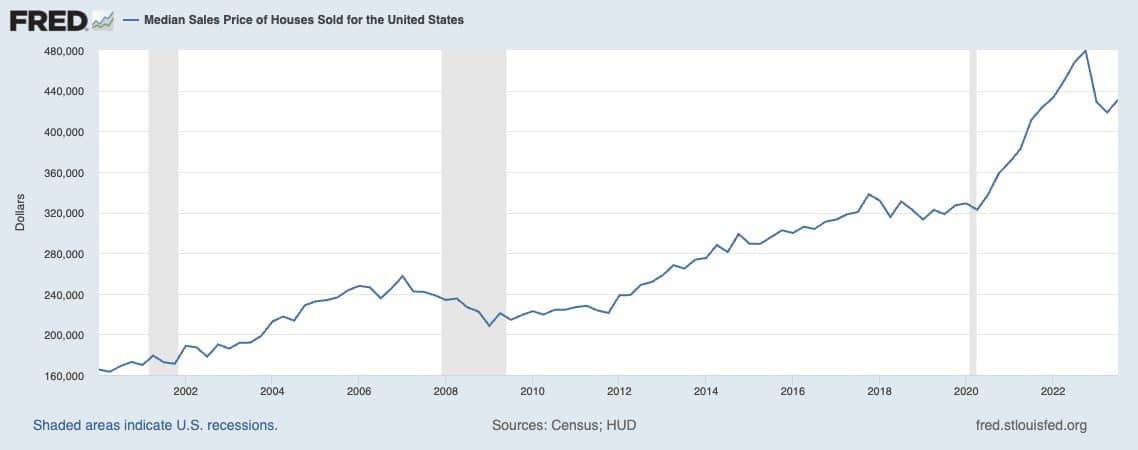

Supply and demand will drive market pricing.

When supply is low, prices go up. When demand is high, prices go up. But when supply is low and demand is high prices take off. Below are two graphs from January 2000 to now. The first is the available supply of homes, the second is the median sales price of available homes. These graphs illustrate this concept.

What jumps out is the available homes graph currently trending down, while the median price graph is currently trending up. I believe that these will continue in their current direction for the foreseeable future.

The two driving factors for this are:

1. The number of current homeowners locked into a sub 3.5% rate.

2. The lack of risk-taking by builders over the last decade-plus in building new homes after the crash of 08-10′.

We’ve known, probably since 2015, that the market was heavily undersupplied which was the launching pad for the housing market when the rates were cut by the FED during Covid. This created higher demand. It was a low-supply, high-demand era. Do you remember what happened with home prices?

We are still undersupplied. The difference this time is that when, not if, but when the rates are cut, the supply will be even drastically less because of the number of homeowners with such historically lower rates unwilling to move.

The future of the housing market: You Haven’t Seen Anything Yet.

If you thought the crazy ride of 2021/22 with home prices was insane, well then buckle up buttercup, because it’s about to get wacky.

As I said at some point the FED will cut rates and when they do all the people on the sideline will come rushing to the market. Those who could not swallow the higher rates will begin leaping at the chance to buy a home, and most have had the extra time to save up more cash.

Take into account the lack of buying in the age group that was coming of age to buy during high-interest times and you squeeze that supply even more.

I say this with full confidence, but whatever the housing prices are in early 2024 will be the cheapest they will ever be again.

The future of the housing market: What Should You Do?

That’s a hard question to answer. Homeownership isn’t for everyone, but it is an amazing way to build wealth. I will say if you do plan on buying in the next three years, I would do everything possible to do it next year.

Perhaps you aren’t familiar with the 18.6 Real Estate cycle and I won’t go into detail here. But the theory, simply put, is that the market goes through cycles of about 18.6 years and this has been tracked for multiple cycles. Check out the graph above to see where we are in the current cycle. We’re getting ready to head into that explosive phase that will then send us into a crash.

If you own a home now, you have nothing to worry about. If you’re buying in the next 12-18 months, nothing to worry about. Anything past mid-2025 and you need to do some soul-searching on your equity.

As I said, throughout 2024 until QE is in full swing your investment, I believe, is safe. I do not think {and as I said this is dubious speculation} your investment is at risk. Once QE ramps up and the market takes off, your risk will grow with the market.

Now does that mean no one should buy in the last four years of the cycle? Absolutely not. Ashley and I are already planning to buy during that phase and are actually putting together some investment groups to take advantage of the housing correction that’s coming. You see, once the correction happens a new low will be created. Most likely not lower than now or what we’ll see in the immediate future, but a new bottom, per se.

And let’s be clear that when the crash happens, it doesn’t have to take four years to reach the bottom. As seen below, 2 cycles ago it did so within the year and the last cycle did most of its drop within the first year, as well.

The obvious risk is that if you buy at or near the peak then you lose several years of equity growth as you wait for the market to catch back up. But if you buy after the “big drop” then you preserve that equity and minimize your downside risk.

So what should you do? Honestly, that depends on your personal situation. But now at least you have a few more tools in the toolbox to help you.

As we have said, if you are buying, selling, or interested in getting involved in the Real Estate market in Nashville reach out to us we’d love to help you. And if you just need help with finding a good real estate agent where you are or where you are moving to, we’d be happy to help you do that as well!

You can sign up here so we can start the process. And even if you aren’t in Middle Tennessee, contact us here, and we will take care of you no matter where you live. There is no reason to go it alone.

Have an inspired day!