tips for buying a home in a high interest-rate environment

We’re thrilled to be back with another real estate post today, and thought we’d tackle this little topic: tips for buying a home in a high-interest environment! We’re so excited to share our experience. If you’re in the market now or will be in the future, we want to provide you with valuable information for navigating the real estate market. And whether here in Nashville or throughout the country we can help you make that next purchase!

Let’s dive in.

The housing market is, for lack of better words, weird right now. We are in this odd environment where lots, and I do mean lots, of homeowners are in a sub-3 % interest on their mortgage and all most all homeowners are sub-5 % interest on their mortgage. So the market is moving at a snail’s pace because essentially, no one wants to give up the rate they have.

Combine what people view as high-interest rates, with high sales prices and potential homebuyers feel hopeless. So what is one to do that either “needs” to move or “wants” to move?

Today we want to give you 5 tips for buying a home in a high-interest-rate environment. {If you’ve missed any of our other real estate posts make sure to check them out for some valuable information. And if you just love checking out real estate in the Nashville area, have fun with this tool.}

before

1. 5 Tips for Buying a Home in a High-Interest-Rate Environment: Adjust Your Perspective

This first tip is all about adjusting your perspective, because there are and have been a lot of people who were thinking rates would be going down by now, but the honest truth is the 6-7% rate is here to stay for a while. Don’t be surprised if we hit 8% by the end of the year.

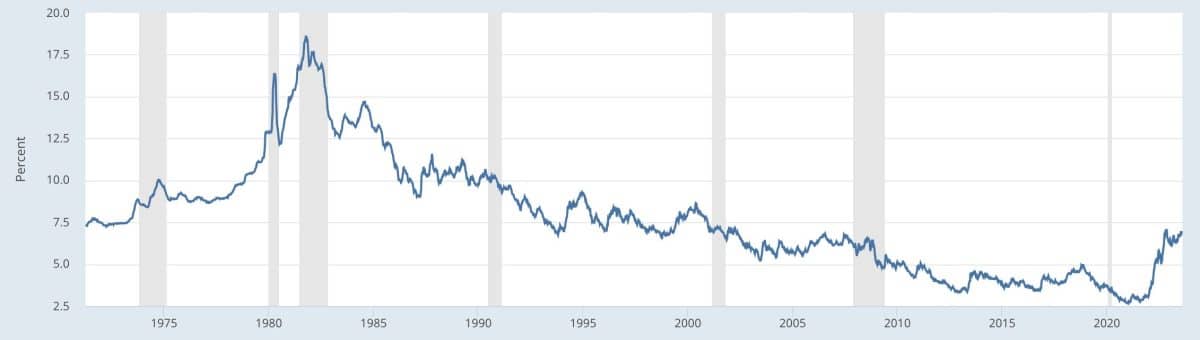

No one can deny that the mortgage rates are high compared to what they were in 2021. But when you look at the data you also can’t deny that historically, they aren’t overwhelmingly high. In fact, they’re average.

In the three decades prior to 2000, mortgage rates didn’t dip below 7% until 1998. And we didn’t see real staying power below 5% until the 2010’s. But therein lies the problem: there’s a good chance that a vast majority of people who are reading this post didn’t buy their first home before 1998. So those plus 7% mortgage rates are crazy talk.

The average rate from 1971 until 2023 is 7.74%, so anything below that is below the historical average. That doesn’t mean you have to like it. That doesn’t mean it has to make you feel good. And it doesn’t change a thing, other than your perspective. For what it’s worth, as of the writing of this post, a 700 credit score would earn you a 6.8% 30-year mortgage rate. An almost whopping full point BELOW the historical average.

So here’s your perspective: the sky is not falling, and we have a long way to go before it does. You can talk to the new home buyers from October of ’81 with their +18% interest rates. {Ouch!} Short term, however, the rates will stay higher than they were, most likely not higher than average for long, just higher than 2021. Eventually, they should go back down some. This is also another reason you shouldn’t be shocked if they go to 8% this year. That alone gives the FED the ability to “lower rates”.

2. 5 Tips for Buying a Home in a High-Interest-Rate Environment: Let Go of the Expectations and Renovate

Even more, than that, look for a smaller house and add square footage. We can say this ’til we’re blue in the face, but when we purchased our current home, we purchased it after living in two prior homes when we were the first owners of the home. So, they were brand new. Going from that to something built in 1976 that needed a ton of work, was an adjustment for us. It was 1690 square feet and had only 3 bedrooms.{There are five in our family, so the kids shared spaces for a whlie.} 18 months later, it became 2,450 square feet. Then we added on again it turned into 2900 square feet. 18 months after that, we built a 250 sqft cabana by the pool for the kids to hang in with friends, and finally {yes, it required some patience with codes and finances} we took it to +3700 sqft 2 years later. So in about 6 years and with a dream in mind, we over-doubled the size of our undervalued house.

Here is why that matters: we paid X (our initial investment) for the house we purchased, but if we would’ve bought a 3700 sqft home at that time we would have paid X + 5. Instead, we bought a smaller house with a 6-year dream and our investment was X + 2 over those 6 years for the same size house and we got to build it like we wanted.

But it gets better

If we would have bought a 3700 sqft home back then, today it would be worth our initial cost of the home + 4.

The smaller home we did buy and added to, is now worth our initial cost of the home including our renovation cost + 8.

So we are +4 by buying the smaller home and renovating it. That is a heck of a difference!

I simply say that to say time is on your side if you have patience, a vision, and adjust your thinking. It can be easy to feel limited in this market. If you need help with the vision part whether here in Nashville or across the country, feel free to reach out to us, we love helping clients.

3. 5 Tips for Buying a Home in a High-Interest-Rate Environment: Financing Creativity

Whatever goes up must come down. As we’ve said here before, financing doesn’t have to be forever. It is only plausible to think that rates will eventually start coming down, so don’t feel like you’re married to the rate you get today. You can always refinance it when the rates begin to drop.

ARM or adjustable rate mortgage is one way to help swallow the pill of higher interest now. This can be a way to lower your monthly payment by reducing the interest rates now. And in 5, 7, 10… or however many years from now your ARM expires you can weigh your options of sticking with the adjustable rate or refinancing.

Does the current homeowner have an assumable mortgage? This is another thing people don’t consider. Most everyone refinanced over the last 3 years, so if they do, it will most likely be significantly lower.

Seller financing is another, more rare option to explore. This is where instead of getting a loan from the bank you essentially borrow from the seller, which might allow you to negotiate a better rate.

Buying points against your mortgage. You pay more up front, but if you will be in your home for a long time, it very well could save you in the long run.

4. 5 Tips for Buying a Home in a High-Interest-Rate Environment: Location and Size

If you want or need to buy a house, then you need to ask two very important questions, what are the up-and-coming locations, and what are the projected home sizes people will want in this area moving forward? {HINT: it is not a McMansion.} This is simply to maximize your investment. Because after all that is the biggest function of buying a home.

In a high-interest rate era, you want to make sure you’re buying in a location people will want to live in 5-10 years and that the size home you are buying is the size they will want/can afford. This will help set up the possibility of getting the maximum price rise for the home. Because while you might have to pay higher interest on the loan if your average rise in home value exceeds that interest, you are effectively protecting your investment.

If, however, you buy in a location that doesn’t rise as quickly you could lose money.

For argument’s sake, we are going to assume the best interest rate we will see over the next 10 years is 4.5%. You take out a 7% loan today for the new house. As long as your home value grows by 4.73% (2.23% average inflation rate over the last 30 years + 2.5% or the difference between your 7% loan and the assumed best loan of 4.5%) then you will not be losing any money on the higher interest rate with a home value rise of 4.73% when compared against the “best possible” rate over the next 10 years.

However, if your home only grows by 3.5% every year, then you are essentially losing 1.23% of your home investment value every year or over 6% of your investment value over 5 years against the “best possible” rate over the next 10 years.

On the flip side, if you buy in the right location with the right type of home and your home rises 6.5% every year then essentially you gain 1.77% or 8.85% over 5 years on your investment, even with higher interest rates. (Actual monetary growth when factoring inflation in.)

To make it simpler, by picking the wrong location your assumed rate would actually be 8.23% vs picking the right location your assumed actual rate would be 5.23% (both based on a 7% mortgage rate). Talk about cutting rates. That’s a 3% difference.

Even more, that is a difference of almost 15% over five years just by picking the right location. If nothing else, that makes an outstanding case to hire a Realtor to help guide you. Contact us we can help you in Nashville or anywhere else.

5. 5 Tips for Buying a Home in a High-Interest-Rate Environment: Time

Combining all three of the points above, maybe this doesn’t have to be your forever home. Maybe look at it as an investment to help you step into the next home.

If you combine some of the tips above, you can possibly help yourself gain more equity in 3-5 years, which produces a larger downpayment for the next house and in turn lowers your interest rate.

High-interest rates aren’t fun, but when we’re honest with ourselves we realize they aren’t really that high and we have to adjust our thinking away from the easy money era, and back into reality. How do we leave a high-fear environment and operate in a more realistic environment, is the question we should be asking.

________________

Real Estate is an interesting beast and having an agent that can pull the curtains back and help navigate what will most likely be the biggest purchase of your life, is essential. As they say, you don’t know what you don’t know, and that’s where a good realtor comes in. {If you need help in hiring a Realtor, check out our post here.}

If you’re in the Middle Tennessee area I’d love to meet you and help you find the perfect home, you can sign up here so we can start the process. And even if you aren’t in Middle Tennessee, contact us here and we will take care of you no matter where you live. There is no reason to go it alone.

Be sure to check out the rest of our real estate series, here.

Contact us here to work with us + here to talk all things renovations!

Have an inspired day!