now that the rates have dropped

We’re thrilled to be back with another Real Estate post today. If you’ve missed any of our previous posts where we discuss the buying process, what to look for, how to find an agent, and so much more, be sure to check them out here as you start your real-estate journey. If you’re in the market now or will be in the future, we want to provide you with valuable information for navigating the real estate market so we can help you make that next purchase.

But first, let’s keep all the legal guys and gals happy. The purpose of this series is to explore the housing market and what I believe we can expect from it. Please understand we’re not offering personal financial advice. We highly encourage you to talk to your local Realtor and licensed financial adviser. {Side note: If you need help finding a good local Realtor, let us know no matter where you live. We have helped several people with this not-so-little task.}

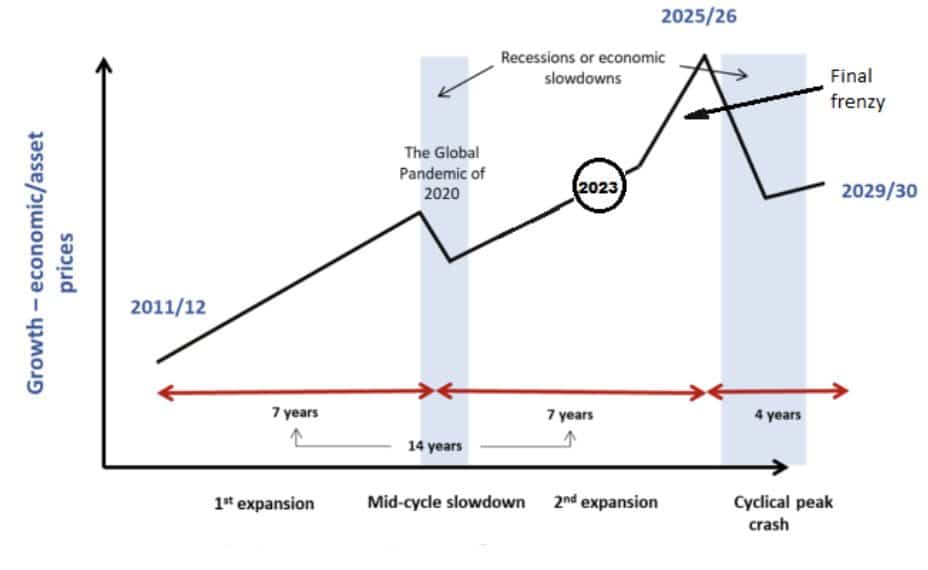

I first shared the two graphs below almost a year ago, laying out what I thought would happen in the Real Estate market and the economy as a whole. There was a lot of fear in the market, and talks were hot and heavy about a recession and a crash. Interest rates were high and scary for many people. If you missed what I wrote back then, I suggest starting here first.

However, the question we want to answer today is, “Now that rates have dropped, should I buy a home?” The simple answer is yes.

In case you missed the news, the FED dropped the FED funds rate by 1/2 percentage point at their last meeting, which, to refresh your memory, means that anything you were looking to get a loan on just became a little cheaper. So, the mortgage for that house you have been eyeing just got a little cheaper. And they are most likely not done cutting rates yet. It is not hard to imagine the FED dropping the FED funds rate another 1/2 to 3/4 percentage points before the end of the year and possibly up to another full point next year.

First Objection to not buying now:

But wait, if I think that the FED will drop the rate up to another 1 and 3/4 points, why would I buy now with interest rates being higher?

To answer that, let’s revisit something I have discussed in previous posts: this does not necessarily mean housing will get cheaper.

Here is the fundamental problem. The housing market is woefully undersupplied, and the principles of supply and demand will drive prices higher as more people come back into the market. So yes, if you wait until next year, then you will most certainly get a better rate. However, the flip side is you will also be paying more for that house as prices will increase as supply is bought up by increased demand due to the euphoria of lower rates bringing more buyers into the market.

And remember, you’re already paying more because of the class action Realtor lawsuit. I’ve been telling clients for over a year that they should buy now and not wait. See: One client who thought I was wrong and believed he knew more. He swore up and down that the market would crash and he could get in cheaper. Let’s just say every single house I looked at with them is now more expensive.

At this point in the rate cycle, you should be heavily considering ARMs (Adjustable-Rate Mortgages) that are convertible to fixed rates. There are two reasons to look at an ARM: first, it gets you into the market before prices go higher, and second, you’re not locked into the higher rate.

Second objection to not buying now:

“But both presidential candidates tell me they will make housing more affordable.” Here’s the truth: I don’t care what you think about either of them. What you need to understand is that the market is way bigger than either of them and that we are in the portion of the market cycle that demands prices go higher.

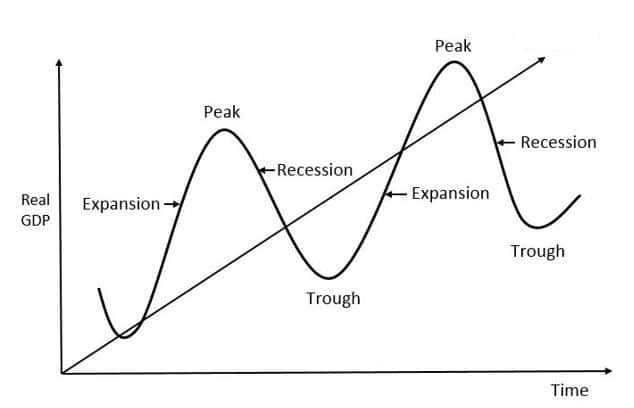

As I have said before, if you plan to own real estate, then turn off Netflix for a couple of nights and learn about the 18 1/2-year real estate cycle.

We are starting the final frenzy, and in this stage, two things are certain.

- Prices will go higher

- A massive correction will happen

This brings about the challenge in this time period of the market cycle, which, simply put, is: Can you buy before the market pushes through what will become the new bottom in the correction? The idea here is that you want to protect your equity. So, if you buy a house for “X,” then you want to be confident that the house will not be valued below that price once the correction happens. Otherwise, as they say, you’re underwater.

As I have said, the longer you wait, the greater the risks you could face, as you could end up on the wrong side of the ledger with your equity. People tend to be short-sighted when making the biggest purchase of their lives. They see interest rates dropping and focus in on that instead of remembering the basic principles of supply and demand, so while they can brag about their lower rate, they won’t be able to brag about their lower price. And in a rate-lowering cycle, which is what we are in, you can always get a lower rate later, but you can’t change the price you paid for the house.

And the correction—that’s the tricky part. No one really knows when it will happen, but we can make an educated guess at where we are in the cycle and weigh the risk v. reward to make the best decision. Personally, I believe now is the time to buy and that you have about another 6-8 months before the risk becomes even or too great.

Third Objection to not buying now:

“Then, should I wait for the crash to buy?” The simple answer is no, not if you can help it. We never really know where the bottom is or how long it will take to get to the bottom. We don’t know if the correction will take one year or four years to reach its cycle bottom. So, if we still have 16-24 months before the correction begins, you could potentially be looking at six years until the next bottom is known. You could be looking at that adorable 6th grader turning into a college Freshman before you get your “dream house” that they were going to grow up in.

Chances are that whatever you pay now is still below the new bottom, and you can deal with that higher rate later. Of course, if you have more time on your hands and you don’t mind where you live currently, then 2030 could be your year.

Final thoughts:

As I have said before, I think we are in or beginning to come out of the trough of the market cycle. We simply don’t know how quickly we get to the peak or how high the peak actually is. I feel confident that a home purchased today will still be a good investment once the correction happens. Ask me again in a few months if buying then is a good idea, and I might tell you a different story.

When you are looking for a Real Estate agent, look for one who is well-rounded and who understands the local market and macroeconomics. I’m also a big fan of finding one who actually knows how a home is built.

If you’re in the Middle Tennessee area, I’d love to meet you and help you find the perfect home; you can sign up here so we can start the process. And even if you aren’t in Middle Tennessee, contact us here, and we will take care of you no matter where you live. There is no reason to go it alone.